The aluminium industry identifies three areas to reduce greenhouse gas emissions.

The report, Aluminium Sector Greenhouse Gas Pathways to 2050, sets out three credible and realistic approaches to emissions reductions for the aluminium industry, in line with the International Energy Agency’s Beyond 2 Degree Scenario. The pathways are based on the IAI’s unrivalled data and leading analysis of the global aluminium industry.

While the industry works to reduce its emissions by about 80%, demand for aluminium products is also predicted to grow. Over the coming decades, global demand for primary aluminium will increase by up to 40% and recycled aluminium from post-consumer scrap will more than triple through to 2050, as economies grow, urbanise, and build up their infrastructure.

Additionally, The International Aluminium Institute (IAI) has modelled a 1.5 Degree Scenario to guide its member’s efforts to meet global climate goals. The modelling is based on IEA’s Net-Zero by 2050 scenario, combined with the IAI’s material flow analysis and future demand scenarios. This scenario is the most ambitious decarbonisation approach and complements earlier work on historical emissions, business as usual scenario (BAU) to the Beyond 2 Degrees Scenario (B2DS).

The Three Pathways

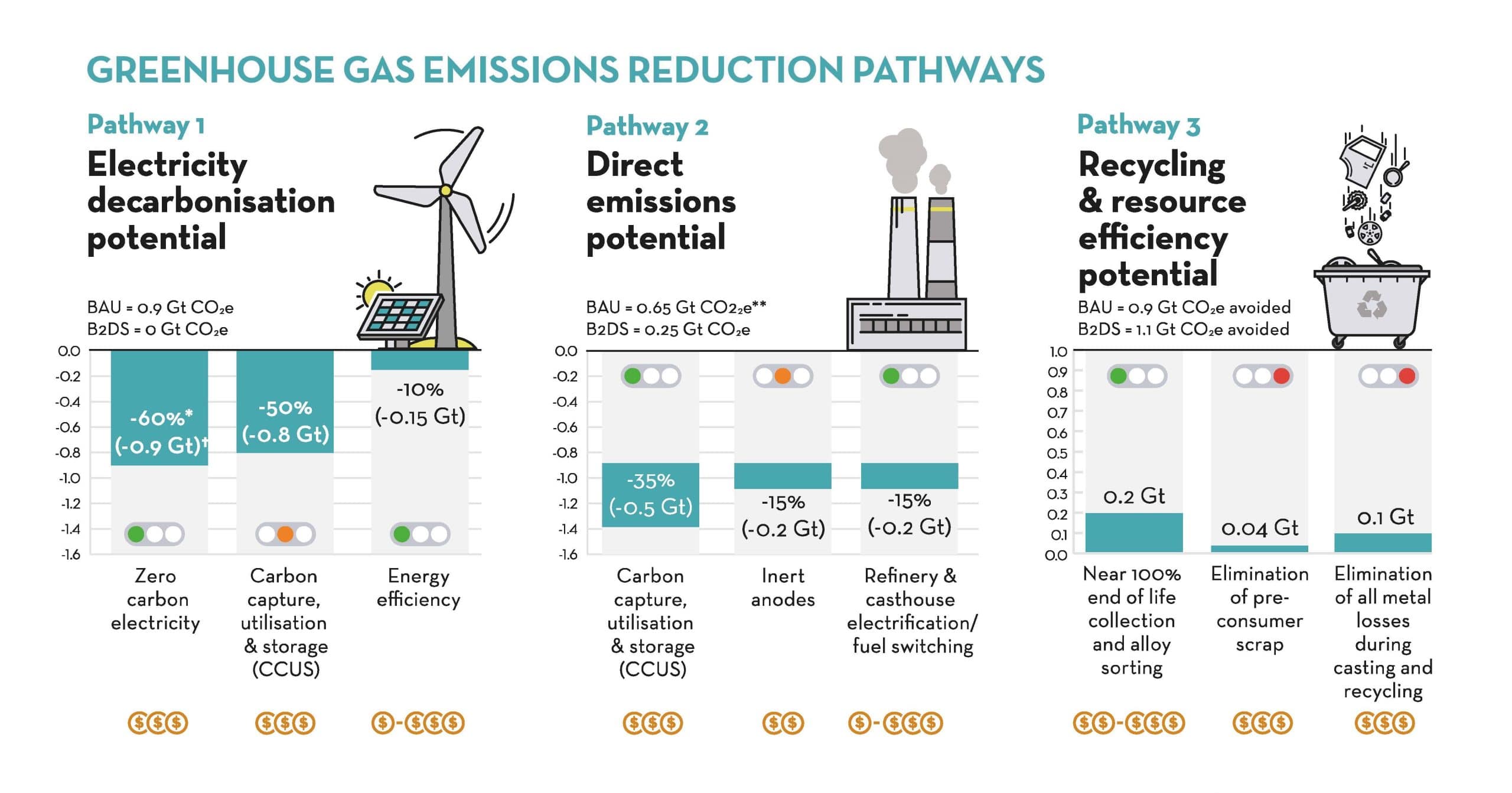

Electricity decarbonisation – Emissions from fuel combustion make up 15% of the industry’s emissions. Here, electrification, fuel switching to green hydrogen and CCUS offer the most credible pathways. Process emissions make up a further 15% and require new technologies, such as inert anodes. These emissions and those in transport and raw materials will need to be reduced by 50-60% from a Business as Usual (BAU) baseline scenario by 2050.

Direct emissions – Emissions from fuel combustion make up 15% of the industry’s emissions. Here, electrification, fuel switching to green hydrogen and CCUS offer the most credible pathways. Process emissions make up a further 15% and require new technologies, such as inert anodes. These emissions and those in transport and raw materials will need to be reduced by 50-60% from a Business as Usual (BAU) baseline scenario by 2050.

Recycling and resource efficiency – Increasing collection rates to near 100% as well as other resource efficiency progress by 2050 would reduce the need for primary aluminium by 20% compared to BAU, which in turn will cut the sector’s emissions by an additional 300 million tonnes of CO2e per year – a figure second in magnitude only to the first pathway, electricity decarbonisation.

The GHG Pathways documents for download include the Report, Executive Summary, Factsheets, an Infographic and underlying data. The Report, Executive Summary and Infographic are also available to download in Chinese.